Business loans play a critical role in helping companies across the United States start, grow, and manage cash flow. Whether you’re launching a startup, expanding operations, or covering short-term expenses, understanding how business loans work can help you make smarter financial decisions and avoid costly mistakes.

This guide explains how business loans function in the U.S., what lenders typically require, how interest rates are determined, and practical tips to improve your approval chances.

What Is a Business Loan?

A business loan is financing provided by a bank, online lender, or government-backed program that must be repaid over time with interest. Unlike personal loans, business loans are designed specifically for commercial use and may be tied to your company’s revenue, credit profile, or assets.

Common Types of Business Loans in the USA

There are several loan options available to U.S. businesses, each serving different needs:

-

Term loans provide a lump sum repaid over a fixed period with regular payments.

-

SBA loans are partially guaranteed by the government and offer lower interest rates and longer repayment terms.

-

Business lines of credit allow flexible borrowing up to a set limit.

-

Equipment financing is used to purchase machinery or vehicles, using the equipment as collateral.

-

Short-term loans offer fast funding but often come with higher interest rates.

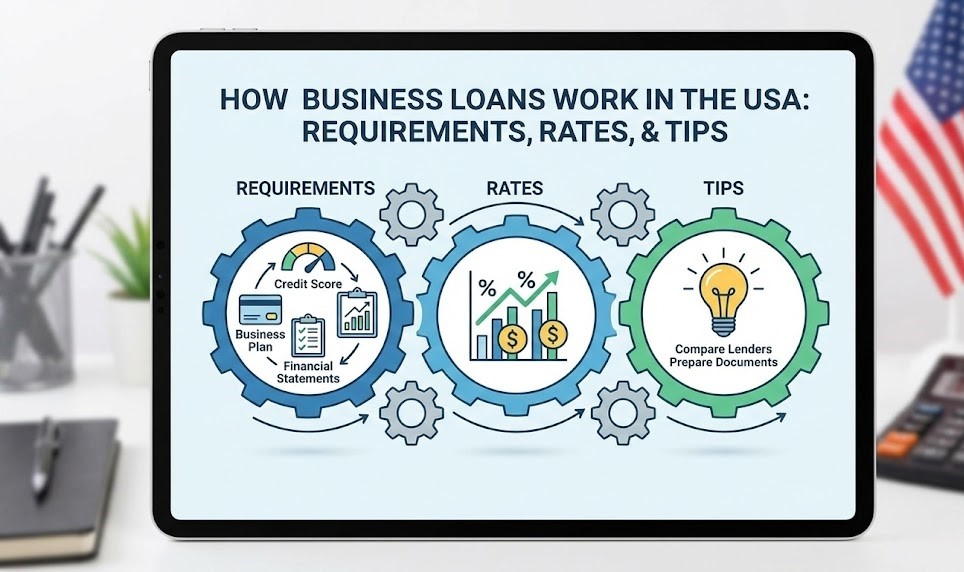

Basic Requirements to Qualify

Lenders evaluate several factors before approving a business loan. While requirements vary, most U.S. lenders look for:

-

A registered and legally operating business

-

Good personal and/or business credit score

-

Proof of consistent revenue

-

Time in business (usually at least 6–12 months)

-

Financial documents such as bank statements, tax returns, and profit-and-loss reports

Startups may face stricter requirements or higher rates due to limited operating history.

Understanding Interest Rates

Business loan interest rates in the United States depend on multiple factors, including the lender, loan type, credit profile, and economic conditions. Rates can be fixed or variable.

-

Traditional banks usually offer lower rates but stricter approval criteria.

-

Online lenders provide faster access but often charge higher rates.

-

SBA-backed loans tend to offer some of the most competitive rates available to small businesses.

A strong credit score and steady revenue typically lead to better loan terms.

How Repayment Works

Repayment terms vary widely. Some loans require monthly payments, while others may require weekly or daily payments. Loan durations can range from a few months to over ten years, depending on the loan structure.

Before accepting a loan, it’s important to understand:

-

Total repayment amount

-

Payment frequency

-

Prepayment penalties

-

Late payment fees

Tips to Improve Approval Chances

-

Build strong credit by paying bills on time and reducing debt

-

Prepare financial documents before applying

-

Choose the right loan type for your business needs

-

Avoid borrowing more than necessary

-

Compare multiple lenders to find the best rates and terms

Being prepared and informed significantly increases your likelihood of approval.

Final Thoughts

Business loans in the USA can be powerful tools when used wisely. By understanding loan types, requirements, interest rates, and repayment structures, business owners can secure funding that supports growth without creating unnecessary financial strain. The key is choosing financing that aligns with your business goals and repayment ability.